Wall Street veteran warns of the impact of high equity exposure

- American households have a high number of stock holdings

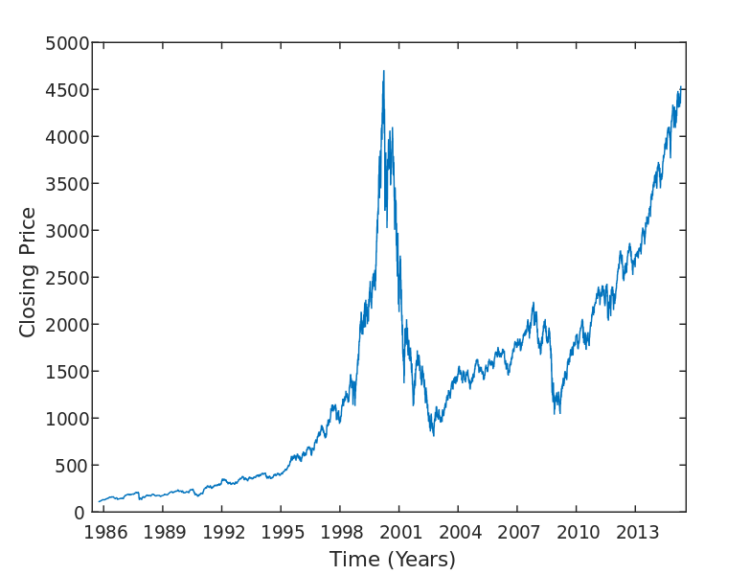

- This could lead to “seven lean years” of returns

- Historically, high equity exposure leads to lower stock returns

- The average long-term household equity share is 25.6%

- Stock returns over the next seven years may be lower than historical averages

Investors are bracing for a preholiday data dump that includes the Fed’s favorite inflation gauge, as the last full week of trading for 2023 closes out. Questions are being raised about whether the midweek plunge in stocks was random jitters, or the start of something more sinister. Stock futures are pointing to another day of losses, as China gaming stocks help dampen the festive mood. Our call of the day comes from a Wall Street veteran who theorizes that based on the high number of stock holdings for American households, investors could be facing “seven lean years” of returns ahead. The U.S. household equity share of total financial assets was 36.3% in the third quarter, Joseph Lavorgna, former Deutsche Bank chief U.S. economist, who now does the same job at SMBC Nikko Securities, told clients in a recent note. That percentage is down from an record of 40.5% in the fourth quarter of 2021, but still well above any other period prior to the current business cycle, he says. Before the pandemic’s onset, the previous record share was set during the internet boom in the first quarter of 2000, with the peak before that 36.9% during the decade’s “conglomerate fad,” said Lavorgna, who also served as chief economist of the Council of Economic Advisers under former President Donald Trump. "Historically, when households own a high percentage of equities in their investment portfolio, future stock returns tend to meaningfully lag historical averages," he said. "Future returns are based on the stock market’s performance over the next seven years because this is broadly consistent with the average length of the post-WWII business cycle," he explains. Lavorgna and his team calculated the average long-term household equity share of financial assets at 25.6%, represented by dashed line in the above chart. High or low household exposure is determined by one-standard deviation bands around that long-term average, shown as solid lines. "From 1952 to 2016, the long-term total annualized return of the S&P 500 including reinvested dividends is 11.4%. However, when the household share of stock holdings is one standard deviation above its long-term average, stocks return just 4.1% annualized over the proceeding seven years. The opposite is true when the household share of stocks is below its long-term average. Stocks return a large 16.0% annualized over the next seven years," he said. The S&P 500’s total return through November is 22.9%, and well above the market’s long-term annual average, he says, but notes that the cumulative annualized return since 2016 is 11.4%, equal to annual returns from 1952 to 2016 period. While the ratio stood at 31.9% in the fourth quarter of 2016, if history holds, Lavorgna says "stock returns over the next seven years should be much lower than the historical average of double-digit gains."

Public Companies: Deutsche Bank (DB), SMBC Nikko Securities (), Council of Economic Advisers (), Nike (NKE), Adidas (ADS), Puma (PUM), NetEase (9999), Tencent (700), Tesla (TSLA), Rocket Lab USA (RKLB)

Private Companies:

Key People: Joseph Lavorgna (former Deutsche Bank chief U.S. economist, now at SMBC Nikko Securities), Donald Trump (former President), Elon Musk (CEO of Tesla), Cathie Wood (CEO of ARK Invest), Jan Hatzius (Chief Economist at Goldman Sachs)

Factuality Level: 7

Justification: The article provides information about the potential impact of high household equity exposure on future stock returns based on historical data. It includes quotes from a Wall Street veteran and presents data on the U.S. household equity share of total financial assets. The article also mentions the Fed’s preferred inflation gauge and other market news. While the article does not contain any obvious misleading information or sensationalism, it lacks depth and analysis, and some of the information provided is tangential to the main topic.

Noise Level: 3

Justification: The article contains mostly noise and filler content. It provides some information about stock market trends and predictions, but it lacks scientific rigor, evidence, and actionable insights. The article also dives into unrelated territories such as gaming stocks and AI research, which are not relevant to the main topic.

Financial Relevance: Yes

Financial Markets Impacted: The article discusses the potential impact of elevated equity exposure on future stock returns for American households.

Presence of Extreme Event: No

Nature of Extreme Event: No

Impact Rating of the Extreme Event: No

Justification: The article focuses on the potential long-term impact of high equity exposure on stock returns, but does not mention any extreme events or their impact.

www.marketwatch.com

www.marketwatch.com